S&P Global Mobility: November auto sales continue previous three-month trend

Ongoing economic headwinds indicate no news could be great news

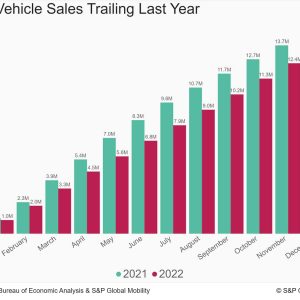

regarding vehicle need levelsWith volume for the month forecasted at 1.122 million units,

November U.S. automobile sales are estimated to equate to an approximated

sales speed of 14.1 million systems (seasonally changed yearly rate:

SAAR). This would represent a continual enhancement from the May

through September period but will show a decline from Octobers.

14.9 million-unit pace, according to S&P Global Mobility.

analysis.The daily selling rate metric in November (around 44-45K.

each day) would be in-line with levels since September. Translation:.

From a non-seasonally adjusted volume standpoint, auto sales.

continue to plug along at a steady rate.” Sales need to continue to improve, offered the anticipated continual,.

but mild, improvement in general production and inventory levels,”.

said Chris Hopson, primary analyst at S&P Global Mobility.

” However, we also continue to keep track of for signals of.

faster-than-expected growth in inventory. Presently, there are no.

clear signs; stocks have advanced as prepared for. Any.

sign of faster than forecasted development in the general stock of.

brand-new cars could indicate that automobile consumers are feeling the.

pressure of the present economic headwinds and pulling away from the.

market.” As a result, Octobers SAAR boost is likely to be an anomaly.

compared to the rest of the year, Hopson stated, including that.

there are expectations of volatility in the regular monthly outcomes.

beginning in early 2023. Market share of battery-electric lorries is anticipated to reach.

5.9% in November. Nevertheless, outside of the large seaside cities,.

retail registrations of EVs have yet to take hold, according to.

analysis from S&P Global Mobility.The top-eight EV markets in the US are all in coastal states and.

represent 50.5% of total EV registrations up until now in 2022 (through.

August). The greater Los Angeles and San Francisco urbane.

areas alone represent nearly one-third of total share of the United States.

EV market. The Heartland states market share of EV sales.

is barely half of what they add to general automobile.

registrations.” BEV market share control on the two coasts is attributed to.

their higher mix of early adopters compared to buyers in middle.

America,” said Tom Libby, associate director of Loyalty Solutions.

and Industry Analysis at S&P Global Mobility. “Their.

group profile is more in sync with the standard BEV purchaser.

than the middle-American profile.” But Libby sees potential for EV acceptance in leading heartland.

markets: “More acceptance and much more comprehensive consumer awareness is.

resulting in a natural development of adoption from the coasts to.

the Heartland.” (For more on this analysis of EVs in the Heartland,.

please see.

this unique report.) Supporting the EV advancement, product reveals surrounding the.

Los Angeles Auto Show last week continue to reflect the OEM.

focus.According to Stephanie Brinley, associate director of.

AutoIntelligence at S&P Global Mobility, “As automobile programs at.

their best highlight what individuals will be driving in coming years,.

the reveals during the Los Angeles Auto Show show the continuing.

push towards electrical and amazed automobiles.” Of note, Fiat revealed it will bring a variation of the European.

500 EV to the U.S. beginning in early 2024, reviving the 500e.

nameplate. Toyotas expose of the 2023 Prius hybrid included a.

Prime trim that will double the hatchbacks EV-only range, while.

the automaker also showed a rendering of the bZ (” Beyond Zero”).

electric-vehicle idea, previewing an upcoming compact SUV.

Vietnamese entrant VinFast showed U.S.-trim versions of.

two EV crossover additions to its lineup – bringing its capacity.

US offerings to 4.

This post was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Leave a reply