S&P Global Mobility predicts strong monthly SAAR for October

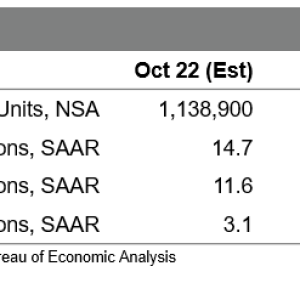

On predicted volume of approximately 1.139 million systems, US

car sales in October will reach a seasonally changed yearly rate

( SAAR) of 14.7 million systems, according to S&P Global Mobility

estimates. While this would mark the greatest regular monthly SAAR level

in 8 months, the underlying dynamics of the marketplace remain in

flux.” Pockets of lorry inventory levels continue to improve

faster than gotten out of extremely low levels and

bring welcome news on the supply side of the formula.

car consumers are likely feeling the pressure of existing financial

headwinds,” according to Chris Hopson, Principal Analyst at

S&P Global Mobility. “While we continue to point to

stock levels as a significant element in stemming immediate-term

momentum in vehicle sales levels, the weakening economic

conditions are becoming more common.” Hindered by greater rates of interest settings and lower levels of

jobs growth than formerly prepared for, customers are expected to

retrench – thus becoming a significant input element to car demand

levels over the next 12-18 months. In its October 2022 US Economics

upgrade, S&P Global Market Intelligence team has actually revised

downward its forecast of genuine GDP development in 2023 from 0.9% to

-0.5%. The base forecast now includes a mild recession beginning in

the 4th quarter of this year, with an anemic recovery taking

hold in the 3rd quarter of next year.If theres a silver lining, the potential for faster new-vehicle

stock development need to permit for down pressure on car

pricing and provide some clearance for vehicle customers going to

test the marketplace in 2023.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is an individually handled division of S&P Global.

Leave a reply